Facing wage garnishment is stressful, there’s no way around it. You work hard, and the idea of money disappearing from your paycheck can create real worry about how you’ll cover rent, bills, or groceries. Do you know what rights you have in this situation? Have you wondered if you can fight back or at least lessen the impact on your daily life? You’re not alone in asking these questions. Let’s look at wage garnishment from the ground up, so you can feel more in control, make informed decisions, and get the help you deserve.

Don’t Let Wage Garnishment Control Your Life—Shanner Law Can Help You Take Back Your Paycheck

Wage garnishment can feel like an invisible hand taking your hard-earned money without warning—but you’re not powerless. At Shanner Law, we help San Diego residents understand their rights, challenge garnishment orders, and explore legal protections that may reduce or even stop paycheck deductions. Whether you need to dispute an error, file for exemptions, or consider deeper debt relief options, our experienced legal team is ready to act fast on your behalf. Contact us today to take back control of your finances and protect what you’ve worked so hard for.

Key Takeaways

- Wage garnishment occurs when a court or government agency orders your employer to withhold part of your paycheck to repay a debt, but there are legal limits to how much can be taken.

- You have important rights regarding wage garnishment, including advance notice, the ability to dispute the debt, and protections against unlawful job termination.

- Wage garnishment legal aid can help you challenge errors, negotiate with creditors, and ensure you benefit from all applicable exemptions.

- Acting quickly—by reading all notices, checking for mistakes, and contacting legal aid—can protect your rights and reduce the garnishment’s impact.

- Proactively communicating with creditors and seeking legal advice early on can help prevent wage garnishment or resolve it more favorably.

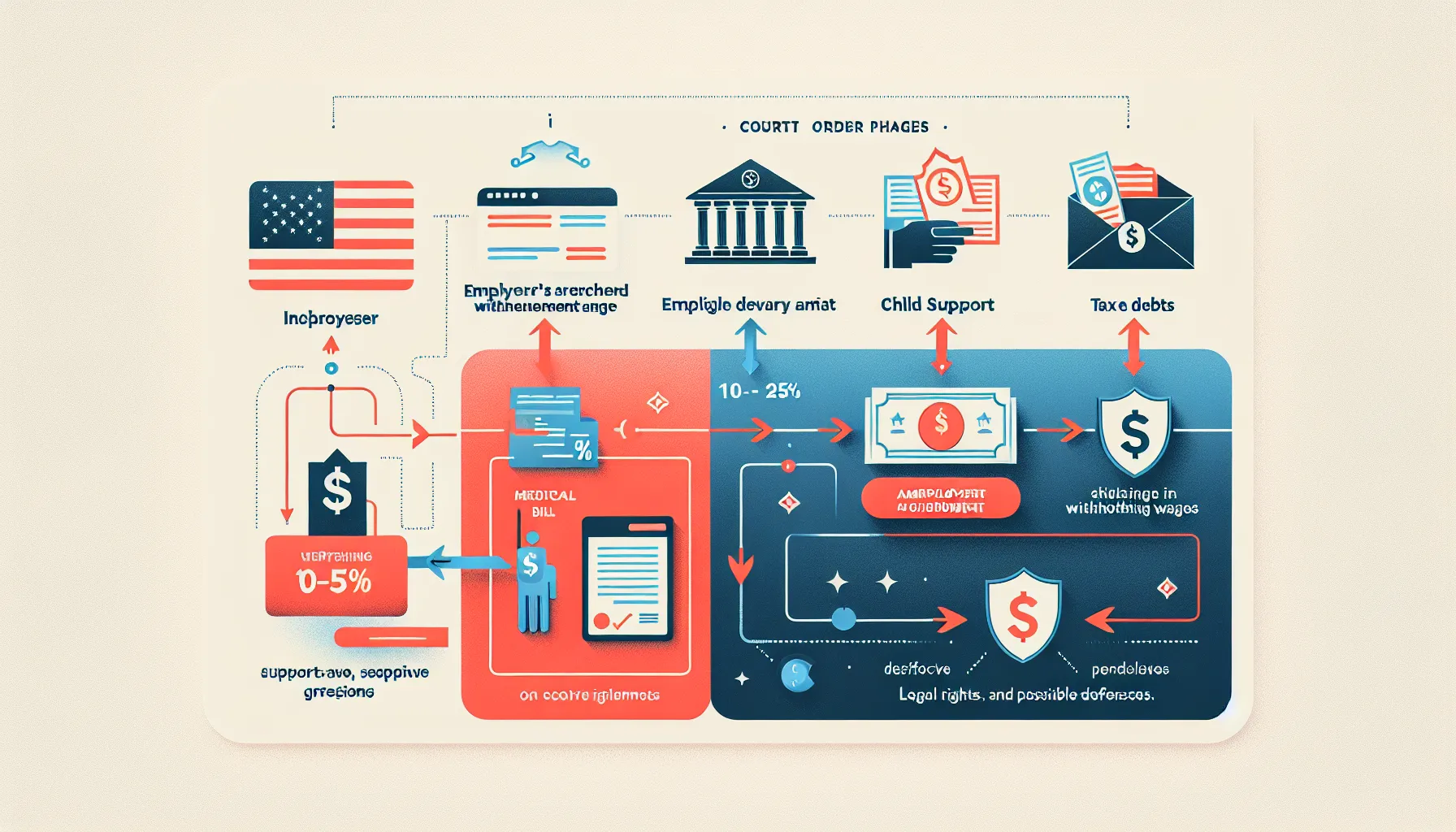

Understanding Wage Garnishment

diagram showing wage garnishment process and protected employee rights in the US

Wage garnishment happens when a court or government agency orders your employer to withhold a portion of your paycheck. That money goes directly to repay a debt, such as a past-due loan, unpaid taxes, child support, or medical bills. For many, wage garnishment feels sudden, but it’s usually the end of a longer process. Creditors often have to sue and win a judgment before taking this step, though some government debts can trigger garnishment more quickly.

The amount that can be taken is limited by federal and state law, so you won’t lose your entire paycheck. Instead, a percentage, often between 10% and 25%, will be withheld, depending on your income and the type of debt involved. It’s important to remember: garnishment is a legal process, but it’s not the end of the road. You still have rights and ways to respond.

Common Reasons for Wage Garnishment

Why does wage garnishment happen? Here are some of the most frequent causes:

- Unpaid credit card debt or loans: Creditors can seek a court judgment if you fall seriously behind.

- Child support and alimony: Courts may order garnishment to ensure these obligations are met.

- Unpaid taxes: Federal and state tax agencies can garnish wages, sometimes without a court order.

- Medical bills: Unresolved medical debt can also lead to lawsuits and garnishment.

- Defaulted student loans: The U.S. Department of Education can garnish your wages for federal student loan defaults, often without a court process.

These situations are more common than you might think. Financial setbacks can happen to anyone, often through no fault of your own, job loss, illness, or unexpected expenses can all leave you struggling to keep up.

Your Legal Rights When Facing Wage Garnishment

Learning your rights is the first, and perhaps the most empowering, step to facing wage garnishment. Did you know that there are strict legal rules about how and when your wages can be garnished?

- Advance Notice: In most cases, you must be notified before garnishment begins. This usually includes a court notice and the right to dispute the debt.

- Limitations on Amounts: Federal law caps how much can be taken from your paycheck. Generally, creditors can’t take more than 25% of your disposable income, or the amount by which your wages exceed 30 times the federal minimum wage, whichever is lower.

- State Protections: Many states have even stricter limits or offer extra exemptions. For example, some protect a larger portion of your income, or certain public benefits.

- Right to Dispute: You have the right to challenge the garnishment in court if you believe it was wrongly issued or the amount is incorrect.

- Job Protection: It’s illegal for your employer to fire you because your wages are being garnished for a single debt.

Understanding these protections can help ease some of the fear around garnishment and lets you advocate for yourself more effectively.

How Legal Aid Can Help with Wage Garnishment

You might be wondering: Can legal aid really make a difference if your wages are already being garnished? The answer is yes, absolutely. Legal professionals offer valuable support for people caught off guard by wage garnishment.

Legal aid attorneys focus on helping those with limited financial resources. They can:

- Review your case for errors: Mistakes do happen, maybe you were never notified, or the debt doesn’t belong to you.

- Help you file objections: If you dispute the amount or validity of the debt, legal aid can guide you through challenging the garnishment.

- Negotiate on your behalf: Sometimes, creditors are open to settling debts for less or arranging a payment plan.

- Explain and apply exemptions: You might qualify for extra protections under state or federal law that reduce or eliminate garnishment.

- Explore bankruptcy and other options: Legal aid can help you decide if bankruptcy or another solution is right for your situation.

If you’re struggling to find affordable help, don’t let that stop you. Many local nonprofits and legal clinics provide free or low-cost services related to wage garnishment.

Steps to Take If Your Wages Are Garnished

Feeling out of control? Start with these steps to regain your footing:

- Read every notice: Make sure you understand what the notice says, who is garnishing your wages, and why.

- Check for errors: Double-check the amount, dates, and debt details for accuracy. It’s not unusual for mistakes to surface.

- Consider your exemptions: Federal and state law may shelter part of your income. You might need to file paperwork or attend a hearing to claim them.

- Respond on time: Deadlines for disputing a garnishment can be short, sometimes just a week or two. Don’t wait to take action.

- Contact legal aid or an attorney: If any part of the process seems unclear, or you think something isn’t right, reach out. You don’t have to handle this alone.

- Communicate with your employer: Let them know you’re aware of the situation. Employers must follow the court’s instructions, but they can also provide paperwork and help explain the deductions.

By acting quickly, you protect your rights and create more space to resolve the garnishment.

Preventing and Resolving Wage Garnishment Issues

What can you do to avoid wage garnishment altogether, or bring it to an end? Here are some strategies that may help:

- Stay proactive: Respond to creditors before they take you to court. Many will offer time to pay back what you owe or settle for a lower sum if you communicate early and often.

- Prioritize essential bills: If you’re in a tight spot, focus first on rent, utilities, and groceries. Many debts can’t be resolved if you lose your housing or utilities, so these basic expenses come first.

- Seek legal advice: Even a brief consultation with a legal expert can give you new insights. Options like bankruptcy, debt settlement, or filing a hardship request may become available through professional guidance.

- Know your limits: Each debt comes with its own statute of limitations. Old debts may be uncollectable, and legal advice can clarify if creditors are within their rights.

- Explore workforce protections: If wage garnishment would cause a genuine hardship, ask about state or federal hardship claims. You may also petition the court for additional relief.

Getting ahead of debt issues and understanding your legal avenues can reduce stress and put you back on the path to financial stability.

Conclusion

No one wants to face wage garnishment, but understanding your rights and knowing you’re not in this alone can make all the difference. Legal aid stands ready to offer genuine support. Whether you’re weighing exemptions, disputing a debt, or exploring relief from overwhelming bills, there’s real hope in taking action. Even a few informed steps forward can change your outlook, and your financial future, for the better.

Frequently Asked Questions About Wage Garnishment Legal Aid

What is wage garnishment and how does it work?

Wage garnishment is a legal process where a court or government agency orders your employer to withhold a portion of your paycheck to repay a debt. The withheld amount is sent directly to the creditor or agency owed.

How can legal aid help with wage garnishment?

Legal aid can review your wage garnishment case for errors, help you file objections, negotiate with creditors, and explain exemptions that may reduce or eliminate garnishment. They can also advise on bankruptcy or other debt solutions.

What are my rights if my wages are being garnished?

You have the right to receive advance notice, dispute the garnishment in court, and benefit from federal and state limits on how much can be taken from your paycheck. It’s also illegal for your employer to fire you over a single wage garnishment.

Can I stop wage garnishment if I act quickly?

Yes. Responding promptly to notices and seeking legal assistance strengthens your chances of disputing errors or claiming exemptions. Acting within deadlines is vital to protect your rights and potentially halt garnishment.

What types of debts can result in wage garnishment?

Wage garnishment can result from various debts, including unpaid credit card bills, loans, child support, alimony, taxes, medical bills, and defaulted student loans. Some government debts may trigger garnishment without a court order.

How can I prevent wage garnishment from happening?

Prevent wage garnishment by staying proactive: respond to creditors early, prioritize essential bills, seek legal help, and know your debt’s statute of limitations. Early communication and legal guidance can help avoid or resolve garnishment issues.